A Guide to Cross Border Payment Solutions for SaaS

When you need to send money across international borders, you're dealing with cross-border payments. This isn't like a simple domestic bank transfer. It’s a complex ecosystem of different currencies, banking regulations, and financial networks that businesses have to navigate to operate on a global scale.

Why Cross-Border Payments Are a Bigger Deal Than Ever

Think of sending money internationally less like a quick bank transfer and more like international shipping for your funds. It comes complete with different carriers (payment rails), customs checks (compliance), and varying delivery speeds (settlement times). For any modern business, especially one paying out affiliates or partners around the world, getting this right is non-negotiable for growth.

The numbers are just staggering. The global cross-border payments market is on track to hit a total value of around one quadrillion dollars by 2024. B2B payments alone are expected to jump from $39.3 trillion in 2023 to an incredible $59.2 trillion by 2031, mostly because global supply chains are finally going digital. The IMF's recent analysis offers even more data on how this market is evolving.

For founders and product teams, this massive growth is both an opportunity and a major headache. If your cross-border payment setup is clunky or inefficient, you'll run into serious problems:

- High Costs: Hidden fees and terrible foreign exchange (FX) rates can quietly drain your profits and shortchange your partners on the other end.

- Slow Payouts: Old-school bank wires can take days to actually land in an account, creating cash flow headaches and frustrating the global partners you rely on.

- Compliance Risks: Every country has its own maze of regulations. Managing Know Your Customer (KYC) and Anti-Money Laundering (AML) rules is a heavy lift and the penalties for getting it wrong are steep.

- Poor Partner Experience: A confusing and slow payout process looks unprofessional. It reflects poorly on your brand and can easily sour relationships with your most valuable partners.

Effectively managing these payments is no longer just a back-office chore; it's a real strategic advantage. Nail this, and you can attract the best talent from anywhere, enter new markets with confidence, and build a business that’s truly built to scale.

This guide will walk you through it all. We’ll break down everything from the different payment types and fee structures to the technical APIs that make modern cross-border payment solutions work. And for businesses that sell products directly, it's also worth understanding the role of a merchant of record, which can handle a lot of the global sales tax and compliance headaches for you.

Your Guide to the Core Payment Rails and Methods

Think of cross-border payments like international shipping. You could use air freight for speed, a cargo ship for volume, or a local courier for that last-mile delivery. Each choice comes with different costs, timelines, and trade-offs. The "highways" that money travels on are called payment rails, and picking the right one is absolutely critical for any business operating globally.

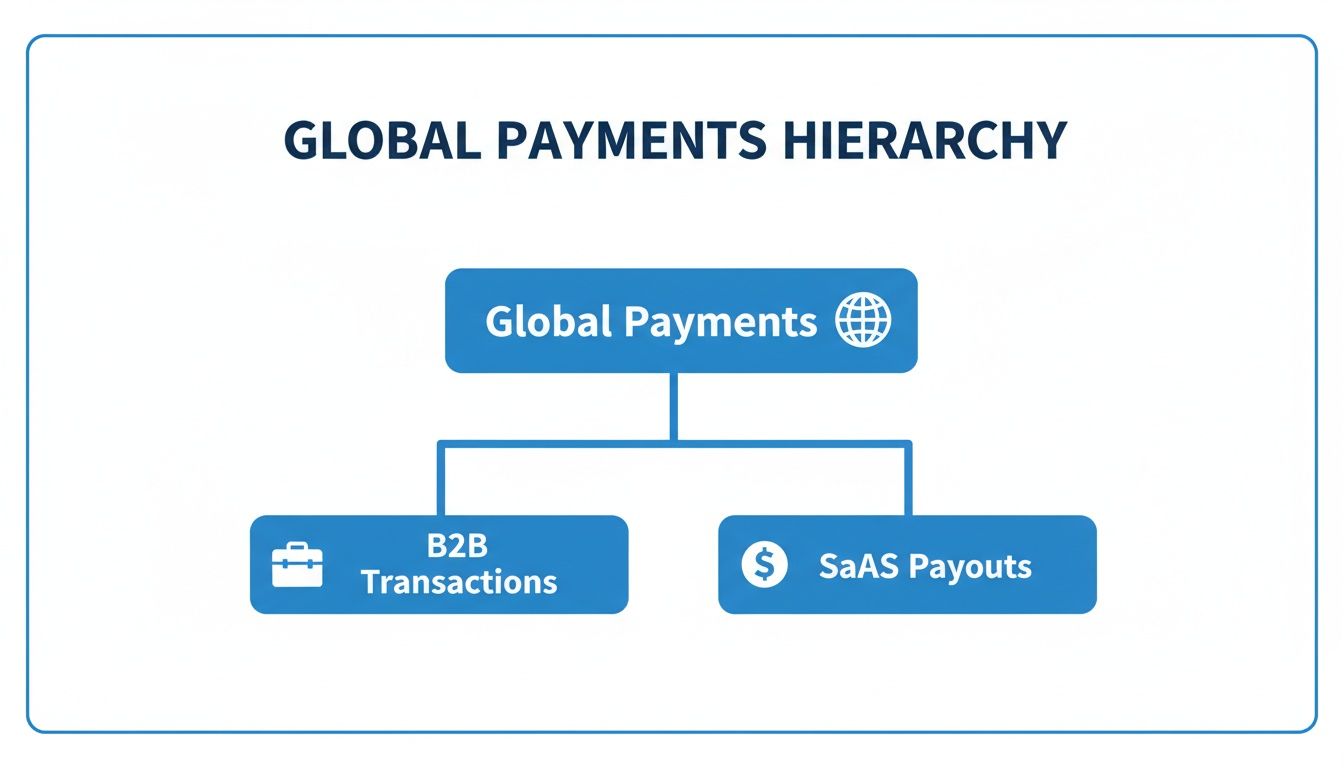

This simple breakdown shows how B2B transactions and SaaS payouts fit into the larger world of global payments.

It’s a good reminder that while these all fall under the "global payments" umbrella, the specific needs of a SaaS platform paying out affiliates are very different from, say, a manufacturer paying an overseas supplier.

The Old Guard: Bank Wires and Card Networks

For a long time, the main highway for big international money movement has been the SWIFT network. It’s the system connecting thousands of banks all over the world. It’s a workhorse for high-value transactions, but it's also famously slow—often taking a painful 2-5 business days—and expensive. The reason for the high cost? Multiple intermediary banks are often involved, and each one takes a piece of the pie along the way.

Then you have the familiar card networks like Visa and Mastercard. They’re fantastic for collecting payments from customers; it's how your users likely pay for their subscriptions. But when it comes to sending money out, especially for mass payouts, they're not always the best tool for the job. Trying to push thousands of individual payments to affiliates through card rails gets complicated and expensive, fast.

The New Kids on the Block: E-Wallets and Local Payouts

Modern payment platforms have figured out how to bypass these older, slower systems. E-wallets like PayPal or Wise (formerly TransferWise) gained traction by building their own networks, which allows them to move money much faster and with more upfront clarity on fees.

But the real game-changer, especially for SaaS and affiliate payouts, has been the rise of local payout networks. This approach is brilliant in its simplicity. Instead of sending a slow, clunky international wire, the payment provider uses its own pre-funded account in the destination country to pay your recipient. The money moves through their local banking system—think ACH in the U.S. or SEPA in Europe.

In essence, this model cleverly turns a complex international transfer into a simple domestic one. The result? Settlement times drop dramatically, often to same-day or even instant, and fees plummet because you've sidestepped the entire correspondent banking maze.

Choosing the right rail really boils down to your specific use case. If you're sending a single, massive payment to a corporate vendor, a traditional wire might still make sense. But if you're like most platforms, paying hundreds or thousands of creators and partners smaller, recurring amounts, a solution built on local payout networks will create a vastly better experience for everyone involved.

Comparison of Cross Border Payment Methods

To make this clearer, let's break down the key differences between these methods. This table gives a quick, side-by-side look at how the most common international payment rails stack up against each other.

| Payment Method | Typical Speed | Average Cost | Global Reach | Best For |

|---|---|---|---|---|

| Bank Wire (SWIFT) | 2-5 business days | High ($25 - $50 per transaction) | Extensive (most banks) | Large, one-off B2B payments where speed is not the top priority. |

| Card Networks (Visa/Mastercard) | 1-3 business days | Moderate (percentage-based) | Very High | Customer payments (pay-ins); less efficient for mass payouts. |

| E-Wallets (e.g., PayPal) | Instant to 24 hours | Moderate (fixed + % fee) | Good, but varies by provider | Quick, small-to-medium payments to individuals with existing accounts. |

| Local Payout Networks | Instant to 1 business day | Low (often a small flat fee) | Growing rapidly | Recurring, mass payouts to affiliates, creators, and partners globally. |

As you can see, the trade-offs are significant. While traditional methods have their place, modern rails like local payout networks are purpose-built for the kind of frequent, global payouts that define the SaaS and creator economies. Your choice ultimately depends on your payout volume, value, frequency, and how much you value your partners' payment experience.

Getting to the Real Cost: FX Rates and Hidden Fee Models

When you start paying people all over the world, one of the biggest leaks in your budget isn't a line item on an invoice. It's the hidden costs baked into the payments themselves. The true price tag of any cross-border payment solution really comes down to two things: the foreign exchange (FX) rate you get and the fee structure you agree to. Getting a handle on both is the only way to protect your profit margins.

Every single international payment involves a currency conversion, and this is where things get tricky. It's easy to get fixated on the obvious transfer fee, but the real damage is often done by the FX rate itself.

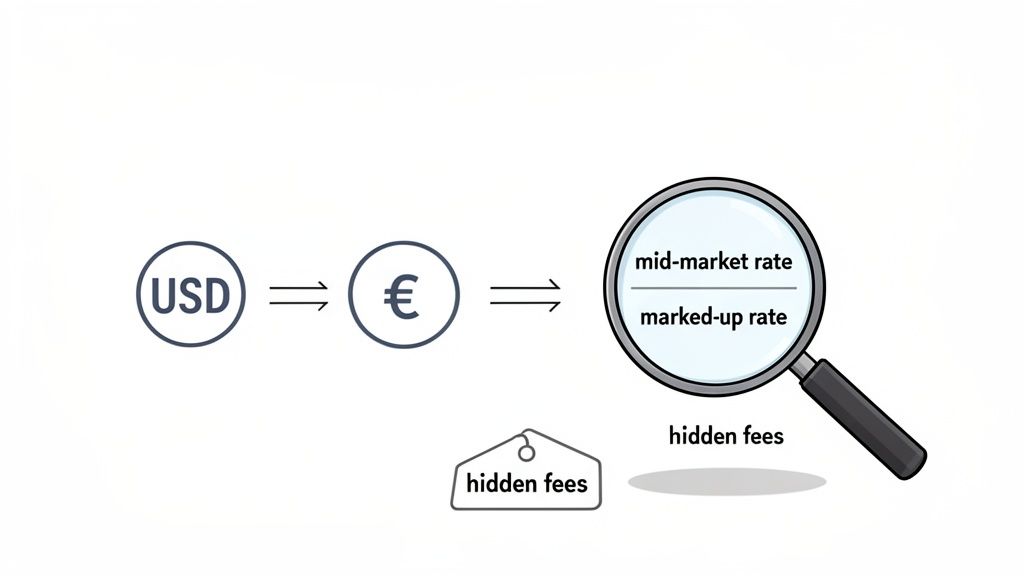

The Mid-Market Rate vs. The Provider's Rate

Think of the mid-market rate as the "real" exchange rate. It's the wholesale price, the perfect midpoint between what buyers are willing to pay and what sellers are asking for a currency on the global market. It's the rate you see when you Google "USD to EUR."

But that’s almost never the rate you actually get.

Instead, most banks and payment providers add a "markup" or "spread." This is a small percentage they quietly add to the mid-market rate, and it’s how they make a good chunk of their money. A markup of 1-2% doesn't sound like much, but it adds up incredibly fast when you're sending hundreds or thousands of payments.

Here’s how it plays out: Let's say the mid-market rate is 1 USD = 0.94 EUR. Your payment provider might offer you a rate of 1 USD = 0.92 EUR. On a single $1,000 payout, that nearly invisible difference just cost you €20. If you’re paying out $100,000 a month, you're losing €2,000 to a fee you never even saw.

As you dig into these costs, it's also smart to look at the bigger picture, including the tax implications of cross border money transfers, which can add another layer of complexity.

Spotting the Different Fee Structures

On top of the FX spread, providers have a menu of other fees they can charge. Knowing what to look for is the key to calculating your total cost of sending money.

- Fixed Per-Transaction Fees: This is a simple, flat fee for every payment you send, no matter the size. It's easy to understand but can be a killer if you're processing a high volume of small payouts.

- Percentage-Based Fees: Here, the provider takes a slice of the total transaction amount. This can work well for smaller micro-payouts, but it gets expensive fast as your transfer amounts grow.

- Landing and Intermediary Fees: These are the worst kind of surprise. They're fees deducted by other banks while a wire transfer (like a SWIFT payment) is in transit. The result? Your partner or affiliate receives less money than you sent, which can lead to frustrating support tickets and a bad experience.

Interestingly, costs are getting more competitive. The global average for B2B transactions recently hit 1.6%, while platform-to-business payments (like SaaS or affiliate payouts) dropped to 1.9%. This shift proves that it pays to shop around. A solid understanding of these costs is your first step toward mastering multi-currency payment processing.

Mastering Global Compliance Like KYC and AML

When you step into the world of international payments, you're not just moving money—you're also a gatekeeper. Before a single dollar, euro, or yen changes hands, there’s a mandatory security checkpoint that every payment provider has to manage. This isn't just red tape; it's a global system designed to stop financial crime in its tracks.

Think of it like a digital passport check at the airport. An agent looks at your ID to make sure you're really you. The financial equivalent is called Know Your Customer (KYC). Payment providers are legally on the hook to run these checks on your recipients before sending them a dime.

It’s a non-negotiable step that’s absolutely critical for preventing fraud.

Why Verification Is Non-Negotiable

This KYC process is a key piece of a much larger puzzle: Anti-Money Laundering (AML) regulations. These are the rules that prevent criminals from using the financial system to wash dirty money. For any business sending payments across borders, a big part of the job is making sure you have solid Modern Anti-Money Laundering Solutions in place.

So, what does this mean in practice? To stay on the right side of the law, a payment provider has to collect and verify some specific info from your global partners, contractors, or affiliates.

- Government-Issued ID: A passport, driver's license, or national ID card is standard for confirming someone's identity.

- Proof of Address: You'll often see requests for a recent utility bill or bank statement to verify where they live.

- Business Documents: If you're paying a company, they'll need to provide things like articles of incorporation to prove they're a legitimate entity.

This whole process is about one thing: confirming your money is going to a real person or a legitimate business. It protects you, your partners, and the entire financial network.

Imagine a SaaS company trying to manage payouts to hundreds of global affiliates. Doing this kind of due diligence in-house would be a nightmare. You'd need a dedicated compliance team and expensive software just to keep up with the constantly changing rules in dozens of countries.

This is where a good payment platform becomes a lifesaver. Modern providers are built to take this entire compliance burden off your plate. They automate the identity checks and screening, letting you pay your global partners securely without needing a law degree in international finance.

By leaning on a compliant partner, you can ensure your payouts are not just fast and efficient, but also completely above board with the strict rules governing how money moves around the world.

Integrating Payouts Into Your SaaS Platform

For the developers and product teams out there, the real magic happens when your payout system feels like it’s part of your platform, not some clunky third-party add-on. Embedding payments directly into your software means your partners never have to leave your ecosystem just to get their money. It’s all about creating that smooth, native experience.

So, how do you pull this off? It comes down to a few core technical patterns.

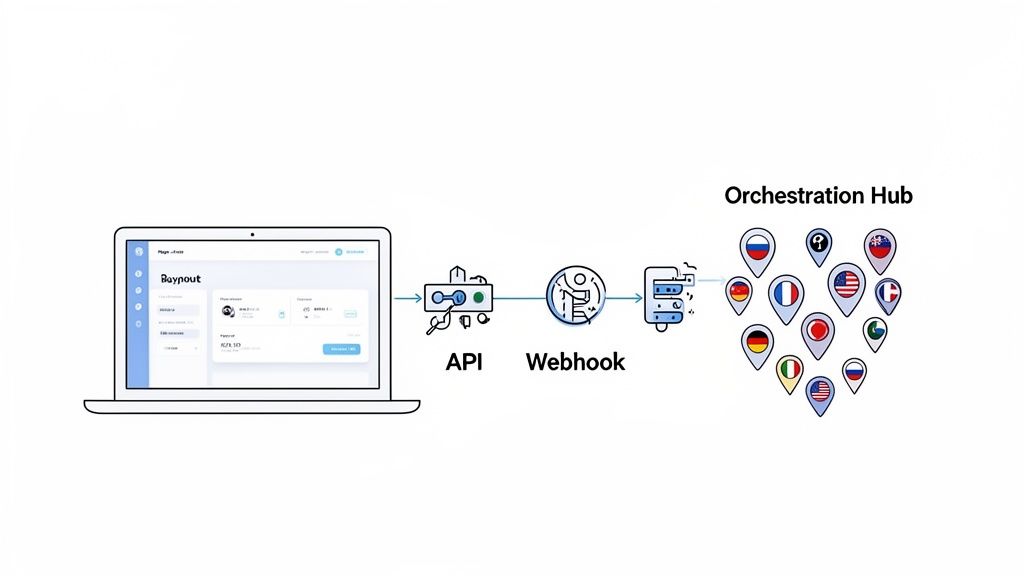

The foundational piece of this puzzle is the Application Programming Interface (API). The best way to think of an API is as a secure, backstage pass. It's a set of rules that lets your application talk directly to the payment provider's system. This allows you to trigger payouts, check their status, and pull transaction history, all programmatically from your own code.

This direct line of communication is what makes automation and scaling possible. It's the engine running under the hood of any modern cross-border payment setup.

Real-Time Updates and Intelligent Routing

APIs are great for sending commands, but what about getting information back? That’s where Webhooks come in. A webhook is basically a push notification for your servers. Instead of your platform constantly pinging the API and asking, "Did that payment go through yet?", the payment provider's system sends you an automatic alert the moment something happens.

This is a game-changer for keeping your users in the loop. With webhooks, you can immediately:

- Flash a "Payment Complete!" message on a user's dashboard.

- Send an automated email if a payout fails because of a typo in the bank details.

- Trigger an alert for your finance team to review a flagged transaction.

For platforms dealing with serious volume, there's an even smarter approach: Payout Orchestration. Think of it as a super-intelligent traffic controller for your money. An orchestration layer sits between your platform and multiple payment providers, automatically choosing the best route for each transaction. It might send one payment via a local partner in Brazil for speed and another through a bank transfer to Germany for lower cost.

This strategy gives you incredible flexibility and resilience, ensuring you’re not locked into a single provider’s network and are always getting the best deal.

The bottom line: When you combine APIs for control, webhooks for real-time feedback, and orchestration for intelligence, you build a payout system that feels like a core feature of your product, not just a bolted-on utility. This is what separates a good user experience from a truly great one.

The global push towards real-time payment systems in over 70 countries is pouring fuel on this fire. As networks like Brazil’s Pix and India’s UPI come online, API-driven platforms can slash settlement times from days to seconds. This shift is empowering money transfer operators to build entirely new services and achieve massive growth.

Want to get into the nuts and bolts? You can explore our payout API documentation to see how our specific endpoints work.

How to Choose the Right Payment Solution

Picking the right cross-border payment solution is more than just a line item in your budget. It's a strategic move that directly affects how you grow globally, how happy your partners are, and how smoothly your operations run. With so many choices out there, it's easy to get stuck in analysis paralysis.

Instead of getting bogged down comparing endless feature lists, let's flip the script. Start by measuring potential partners against what your business actually needs. This checklist is designed to help you slice through the marketing jargon and find a provider that truly fits, whether you're paying your first international affiliate or scaling a massive global marketplace.

Your Core Evaluation Checklist

Working through these questions will give you a rock-solid foundation for comparing different cross-border payment solutions and making a smart decision.

What’s Your Actual Global Reach? Don't get fooled by a big, impressive number of supported countries. You need to dig deeper. Ask them specifically about your key markets and the ones you plan to enter next. Do they offer genuine local payouts (like ACH in the US or SEPA in Europe) in those places, or are they just pushing everything through the old, slow, and expensive SWIFT wire system?

How Transparent are the Fees, Really? This is non-negotiable. Demand a complete, line-by-line breakdown of all costs. You need to know their exact FX markup over the mid-market rate, any per-transaction fees, and—this is a big one—any hidden landing or intermediary bank fees that might surprise your recipient. A partner worth their salt will be upfront about the total cost of moving money from A to B.

What Payout Methods Do You Support? Your partners, freelancers, and affiliates all have their own preferences, and they aren't all the same. A strong solution will offer a healthy mix of options: direct bank transfers, popular e-wallets they already use, and maybe even card payouts. The more flexibility you can offer, the happier your payees will be.

Think about it from their side. A recent study found that a staggering 75% of consumers would switch to a different payment provider just to save time and cut down on fees. Offering the right methods isn't a perk; it's essential for keeping your global talent and partners loyal.

- Can You Grow With Us? Think about the future. Does the provider offer a modern, well-documented API and webhooks that your developers can actually use for a clean integration? Can their platform handle a sudden spike from a few hundred payments to thousands a month without your team having to manually intervene? You need a partner who can support where your business is headed, not just where it is today.

Common Questions Answered

Diving into the world of international payouts always brings up a few key questions. Let's break down some of the most common ones we hear from businesses just like yours.

What’s the Absolute Fastest Way to Pay Someone Internationally?

If speed is your main concern, you'll want to look at modern payment providers that use e-wallets or local payout networks. These rails are built for near-instant delivery, often landing funds in your recipient's account in minutes, or at least on the same day.

We're seeing a huge global push for real-time payment systems, so this is becoming the new standard. On the flip side, traditional SWIFT bank transfers are still the slowest horse in the race, usually taking 2-5 business days to finally show up.

How Can I Actually Cut Down on International Payment Costs?

The secret to lowering costs isn't just about finding the lowest transfer fee. You have to look at the FX rate markup—that’s where the real hidden costs live. Your best bet is to find a platform that’s transparent about its pricing and bases its rates on the mid-market exchange rate.

Another practical tip is to batch your payments. Sending one large transaction instead of ten small ones can dramatically cut down on per-transaction fees. And if you can, work with a provider that has deep local payout capabilities. This helps you sidestep the expensive and unpredictable intermediary bank fees that are so common with older systems.

A recent study found that a staggering 75% of consumers would jump ship to a new payment provider just to save time and money on fees. That really drives home how much cost and speed matter to your global partners and affiliates.

Do I Have to Handle KYC and AML Checks for Every Single Person I Pay?

Thankfully, no. This is one of the biggest weights a good payment partner lifts off your shoulders. As regulated financial institutions, they're on the hook for handling the vast majority of Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance.

Your job is to provide accurate recipient details and to make sure you've picked a reputable, fully compliant provider in the first place. This partnership lets you offload the massive compliance headache, so you can focus on growing your business without worrying about the regulatory red tape.

Ready to streamline your affiliate payouts with a truly native solution? Refgrow embeds directly into your SaaS, offering automated mass payouts, transparent pricing, and a seamless experience for your partners. Get started with Refgrow.